2010: Where was Moody's board when top-rated bonds blew up?

WASHINGTON — As the bottom fell out of the housing market and complex mortgage-backed securities began tanking in 2007, a strange thing happened at Moody's Investors Service, one of the largest firms that rate bonds for the risks they pose to investors.

Moody's blue-ribbon board of directors stopped receiving key information from an internal committee that was supposed to keep the board informed of risks to the company, a McClatchy investigation has found.

Instead, the ad hoc risk-management committee suddenly disappeared, precisely at the time when the board and management should have been shifting to higher alert as the financial world began quaking.

As McClatchy reported last year, the credit-rating agency had been handing out Triple-A grades like candy for Wall Street mortgage securities that were backed by pools of home loans that turned out to be junk.

When the global financial crisis deepened in 2007 and the integrity of bond ratings came under attack, the captains of industry on the Moody's board seldom asked tough questions, according to former Moody's executives who made presentations to the board.

That's important, because the legislation to overhaul financial regulation that's now moving through Congress aims to empower ratings-agency boards by requiring a direct line of communication between the company officials who police for risks and the boards. It's not clear whether that would have made any difference at Moody's.

The findings of the new McClatchy investigation not only call into question the value of the new regulatory approach lawmakers are drafting; they also help underscore the widespread criticism that many corporate boards practice crony capitalism rather than independence.

"My question the whole time has been, 'Where the hell has the board been?'" said a former Moody's employee who was on the disbanded committee. The employee spoke on the condition of anonymity at the advice of a lawyer, fearing future litigation. "I would have expected, sitting where I was, that I would have got a lot more calls from the board. I got none of that."

Several former Moody's executives who made presentations to its board as the financial crisis emerged in 2006 and 2007 described the board members as incurious, saying they seemed to be there primarily to enjoy the perks and prestige of board membership. The former executives all demanded anonymity on the advice of their lawyers.

Moody's board members receive $75,000, $95,000 or $115,000 a year for the six or eight meetings they attend, depending on whether they hold leadership positions, plus $115,002 every year in annual restricted stock.

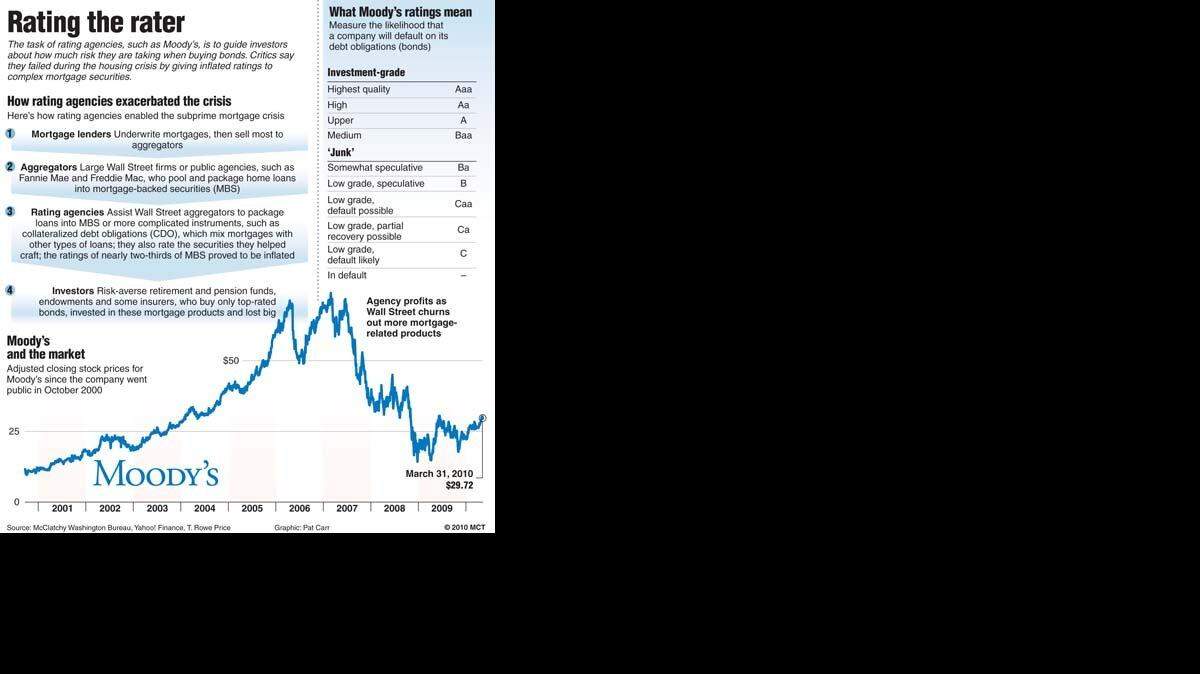

Moody's dominated the ratings for "structured finance" products — securities backed by pools of loans that are packaged together and provide a monthly income stream to investors.

The structured finance division powered Moody's revenues past the $1 billion mark in 2002, and past $2 billion in 2006. The company's stock price soared nearly six-fold between 2001 and 2007, from $12.70 to $72, which created a huge windfall for its largest shareholder, billionaire investor Warren Buffett.

The board, however, apparently had few questions on the way up — or later, on the way down, a former Moody's officials said.

"There was no (corporate) governance at the firm whatsoever. I met the board, I presented to them, and it was just baffling that these guys were there. They were just so out of touch," another former high-level Moody's executive said.

Board members are supposed to protect shareholders, from individual investors such as Buffett to institutional firms that invest the retirement contributions of American workers.

McClatchy also has learned that during this time, as concerns grew about the ratings of complex mortgage-backed securities, two Moody's executives reached out to the company's largest shareholder, Buffett, to warn him of problems.

Buffett's firm, Berkshire Hathaway, based in Omaha, Neb., owned about a fifth of Moody's shares then. It remains the largest shareholder at around 13 percent last year. A Berkshire spokeswoman declined to comment, but a former Moody's employee who reached out to Buffett said the investment guru responded that he was a "hands-off" investor.

McClatchy sent detailed questions twice to Moody's, which recently upgraded McClatchy's debt rating one notch to Caa1 from Caa2; both ratings are considered non-investment, or "junk" grade. Moody's declined to comment for this story, taking issue with McClatchy's use of anonymous sources.

Moody's officials said the comments from former employees provide just a snapshot, not a complete view of the board's activities, but the company refused to provide any detail about what board members did or said during the time in question, and three board members contacted separately declined comment.

At issue is an ad hoc risk committee that was abolished shortly after a management shake-up resulted in the controversial appointment of Brian Clarkson as Moody's president and operating chief in August 2007.

Clarkson was elevated by Raymond McDaniel, Moody's chief executive and the chairman of its board, because of the huge profits coming from the structured finance division.

That division worked closely with Wall Street investment banks such as Bear Stearns, Goldman Sachs and Lehman Brothers to rate mortgage-backed securities.

Big institutional investors such as pension funds and endowments can purchase only top-rated securities, so Wall Street firms desperately needed the blessing of Moody's or its competitors, Standard & Poor's and Fitch.

A McClatchy investigation late last year revealed how Clarkson moved structured finance executives into Moody's top regulatory and compliance positions, seemingly a conflict of interest. The changes also resulted in the firings or departures of numerous executives who'd questioned either the methodologies Moody's was using to rate the complex securities or the risks it was taking.

One veteran who left the company was Chester Murray, the executive in charge of international operations. He headed the ad hoc committee that met quarterly to advise the board on potential threats. After Murray left Moody's in December 2007, the panel never met again, even as the problems in the housing market gave way to what by September 2008 became a near meltdown of global finance. Clarkson announced his retirement months earlier, in May 2008.

Moody's officials wouldn't discuss the ad hoc committee.

"Either the board knew that the risk management committee had been disbanded or they didn't," a former executive said. "If they did know, the question is why they did nothing about it. If they didn't know, it's hard to escape the conclusion that Ray (McDaniel) hid the committee's disbandment from the board, since as board chairman he certainly knew that it had been disbanded."

Moody's rejected requests for McDaniel to comment on the committee or the activities of the board.

"You raise a good question," said Lynn Turner, a former chief accountant of the Securities and Exchange Commission who's criticized the failure of ratings agencies to see the risks in the failed Houston energy giant Enron Corp., which collapsed in late 2001. "I personally think until law enforcement agencies start holding these boards accountable, the point you're raising is probably right on target, and you're probably not going to get a lot of change."

Moody's wasn't alone in making big profits from structured finance and wildly inaccurate bond ratings, and S&P and Fitch suffered similar losses of revenue and reputation when the bottom fell out. Fitch is a privately held company, and S&P is owned by publishing giant McGraw-Hill. After the crisis, both engaged in deeper house cleanings than Moody's did, replacing their top executives.

Moody's chief McDaniel remains on the job, with board support. He was awarded almost $7.38 million in salary and compensation in 2007, the year things fell apart; $7.56 million in 2008 as markets tanked; and $5.4 million last year.

He has his job despite embarrassing October 2008 revelations from the House of Representatives Committee on Oversight and Government Reform. It made public portions of a McDaniel board presentation in October 2007, in which he acknowledged pressure from Wall Street investment banks to give favorable ratings and confided that "at times, we drink the Kool-Aid."

At that same hearing, Jerome Fons, a former Moody's managing director of credit policy, told lawmakers "the deterioration in standards was palpable," adding that managers "turned a blind eye to this, did not update their models or their thinking and allowed this to go on."

Stung, Moody's announced weeks later that it had named Stanford University Finance Professor Darrell Duffie, a well-regarded academic, to its board. Duffie was given a seat on the board's audit and compliance committee.

Reached recently by phone in California, he declined to discuss what transpired before his arrival, but he suggested that corrective steps are being taken by all major rating agencies, including Moody's.

"I'm quite optimistic myself that the rating of structured products is something that can be done well in the future, and that the agencies are positioned to do it well," Duffie said.

Board members are often business icons, sought for the reputational luster they bring rather than expertise in the business of the companies on whose boards they sit.

"The problem is (that) staffing boards often is like decorating a Christmas tree. You get people who are good ornaments, with luster. The question is, do they have the skill set to help the company add value?" said David Nadler, an expert in corporate governance for consultant Oliver Wyman in New York.

The Moody's board includes Henry McKinnell Jr., a former chief executive of pharmaceutical giant Pfizer. He heads the board's governance committee and left Pfizer in 2006 with a "golden parachute" valued at $180 million.

The Moody's audit committee, which oversees compliance, is headed by John Wulff, the retired chairman of chemicals giant Hercules Inc. and a former chief financial officer of Union Carbide Corp. Also on that committee is Basil Anderson, vice chairman of office supplies retailer Staples Inc. until his retirement in 2006 and a former chief financial officer of the Campbell Soup Co.

Former Florida Republican Sen. Connie Mack, who sat on the Senate Banking and Finance Committees, also is on the board. Now an influential Washington lobbyist, Mack retired from Congress in 2000.

The big fish is Robert Glauber, the former head of the National Association of Securities Dealers, a Wall Street self-regulatory body. He was a Treasury undersecretary from 1989 to 1992.

That Glauber allegedly asked so few questions in this turbulent period bothered some who presented to the board.

"He's just the nicest guy, but he was not asking tough questions or digging deeply into what was going on," one former executive said. "That was my impression. I liked him. He had an interesting career, but there was no questioning."

A voice message left for Glauber requesting comment wasn't returned.

Several former Moody's executives said the only tough questions came from board member Nancy Newcomb, a retired senior officer for risk management at Citigroup.

They also described Mack as incurious. He declined comment, citing board duties.

"Senator Mack is another easygoing guy . . . but these people had very little understanding of the nature of the business, how things worked," said a former presenter to the board. "They never walked the floors and talked to the staff. They got the 90,000-foot view of the firm that was highly filtered."

That's what experts feel needs to change on corporate boards.

Unless board members know how their companies operate, they might not ask tough questions.

"Ultimately, a more effective board might have caught what was going on and intervened with management. We don't know," Nadler said. "You can ask the question 'Where was the board?' But the answer could be in a lot of different places."

Because rating agencies earn money from the very people they're rating, there's an inherent conflict of interest. Corporate governance experts think that should mean even greater transparency on their boards.

"I think shareholders deserve some of the fundamentals of how their board is structured and working," Nadler said.

The new legislation contemplated by Congress would expand the number of "independent" members on ratings agency boards and require greater disclosure of potential conflicts of interest and methodology. Moody's and its competitors have already taken steps, albeit after the fact, to make ratings methodology more transparent.

In proxy statements Moody's filed with the SEC in 2006, 2007 and 2008, there's no mention of any action or concerns raised by the board. Annual reports also make no mention of board concerns.

However, the recently filed proxy statement, covering 2009, describes a new risk panel that seems to reinstate some functions of the former ad hoc committee.

The only action the board appears to have taken concerning what went wrong at Moody's was disclosed in the proxy statement to investors for 2008. The board recommended against a failed shareholder proposal from the Massachusetts Laborers' Pension Fund to create an independent chairman for the Moody's board.

The move was aimed at McDaniel, who also serves as board chairman, but it won only 30 percent of the proxy votes. The issue is up for a vote again at the April 20 annual meeting, this time brought by England's Legal & General Assurance (Pensions Management) Ltd.

It's also unclear what the audit committee felt about the departure of experienced audit and compliance executives, who were replaced by colleagues from the structured-finance division.

Months after he became president, Clarkson appointed Michael Kanef, who managed a group in charge of rating asset-backed securities, to be the chief regulatory officer overseeing the compliance staff. Compliance officials began reporting to the people they'd been policing.

According to congressional testimony last year, Kanef forced out Scott McCleskey, the chief compliance officer at Moody's, in September 2008 and replaced him with David Teicher, a structured finance executive with no compliance background. A lawyer with some compliance experience has since replaced him.

"If I had been on that board, as soon as this change was made I would have said, 'What is this person's background?' I would have gone ballistic then and there," said one former Moody's executive who briefed the board.

Senate financial overhaul bill

MORE FROM MCCLATCHY

To ask a question about this story or any economic question, go to McClatchy's economy Q&A

How Moody's sold ratings — and sold out investors

New mortgage plan still has holes, White House concedes

Heartland hurt has many asking: Is China worth it?

This story was originally published April 2, 2010 at 12:01 AM with the headline "2010: Where was Moody's board when top-rated bonds blew up?."