Business fights Obama's fix for sick corporate pensions

WASHINGTON — State and local government pensions aren't the only ones in trouble.

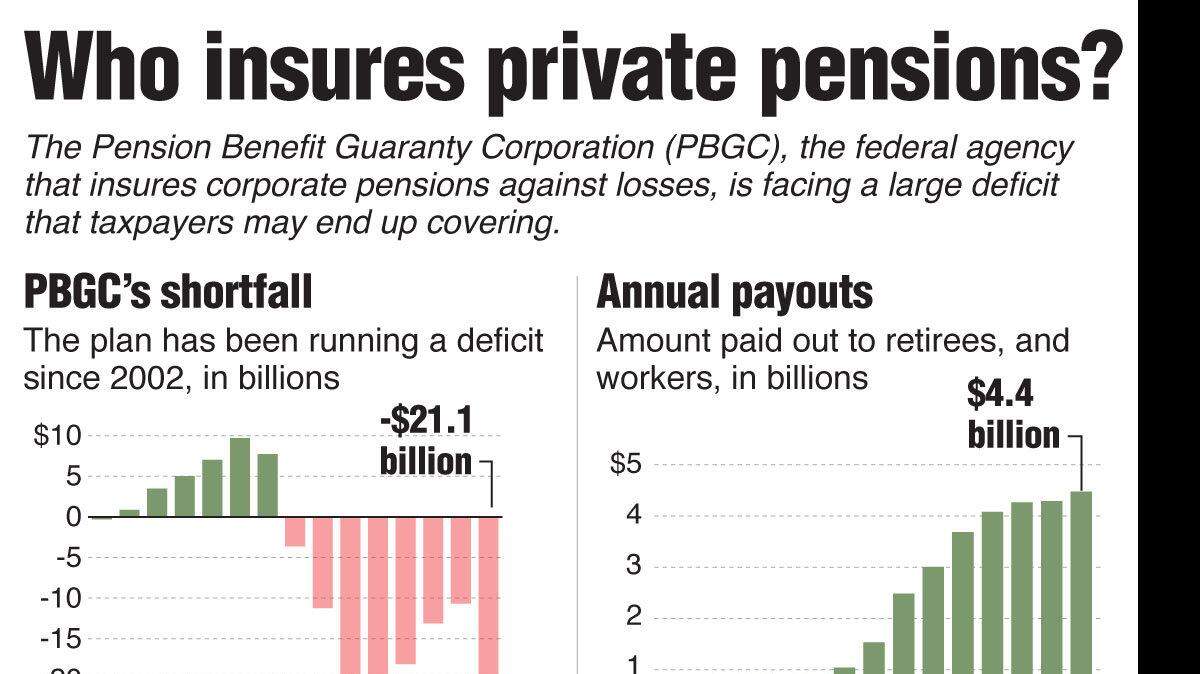

Corporate pensions, too, are woefully underfunded, and the federal agency that insures them against losses is facing a dangerous deficit that taxpayers may end up covering. One government watchdog agency says the federal insurance funds are at "high risk" of failure. Moreover, the Obama administration's proposal to fix this is meeting stiff resistance from the U.S. Chamber of Commerce and other business interests.

The little-known federal Pension Benefit Guaranty Corp. insures roughly 27,500 corporate defined-benefit pensions, covering 44 million U.S. workers. These plans, popular in the public sector but increasingly rare in the private economy, promise workers fixed monthly retirement income, often equivalent to a final year's salary or an average salary over the last few years of work.

The PBGC insures both single-employer plans offered by, say, a large manufacturer, and multi-employer plans, where many companies in a given industry collectively sponsor retirement plans. As of Sept. 30, single-employer plans insured by the PBGC collectively had a deficit of $21.6 billion, and multi-employer plans were in the red by about $1.4 billion.

Single-employer plans had promised more than $121 billion in benefits, but only had assets to pay out $99.4 billion. Multi-employer plans held assets valued at $1.6 billion to cover $3 billion in promised benefits.

When a corporation fails, the PBGC takes over its defined-benefit pension plan. The cost of paying the plan's beneficiaries is supposed to be covered by premiums collected from businesses insured under the federal program.

Two things happened during the recent prolonged economic slump to weaken that system, however. More companies failed and turned over their liabilities to the PBGC; in fiscal 2009 alone, the agency became responsible for another 200,000 workers.

And interest rates have been at all-time lows for more than two years, dragging down the rate of return on bonds. Since many corporate pensions are heavily invested in bonds, rates of return on bonds are used to estimate the value of assets in the plans. The protracted low interest rates have increased the gap between what plans have promised and the value of the plans' investments to cover the promises.

Here's another reason for worry: The PBGC's estimate of "reasonably possible" exposure to failing multi-employer plans soared from $326 million in 2009 to $20 billion in 2010. The same exposure for single-employer plans rose to $170 million in 2010, up only slightly from $168 million a year earlier.

The PBGC says not to worry.

"Because our obligations are paid out over decades, we have more than sufficient funds to pay benefits for the foreseeable future," Joshua Gotbaum, director of the PBGC, insisted in Senate testimony on Dec. 1.

Sound familiar? That's exactly what the National Association of State Retirement Administrators and local government officials now say about the dip in funds available for most of their pension plans — that things will look better over time.

Stuart Hoffman, the chief economist for PNC Financial Services Group in Pittsburgh said that some of the problems facing public and private defined-benefit pensions will ease as financial markets continue to heal.

"If the economy doesn't grow, you can't grow out of your problem," Hoffman said.

The return on investment for the assets under PBGC management rose was 12 percent last year, a number similar to the return for state pensions as the bounce back on Wall Street help lift all investors. The PBGC funds itself through investments and insurance premiums.

However, in a hard-hitting report to Congress on Dec. 1, the Government Accountability Office designated both PBGC insurance programs as at a "high risk" for failure. The GAO said that even if financial markets rise in value and lift investments made by pension plans, the PBGC is "likely to remain at financial risk" because of structural issues.

The GAO, the investigative arm of Congress, said the PBGC can't adequately manage its risks because it "cannot decline to provide insurance coverage or adjust premiums in response to actual or expected claims exposure."

PBGC lacks authority to raise premiums on its own. Historically, Congress has raised premiums so the PBGC can adequately insure against losses.

In its budget released last month, the Obama administration proposed giving the PBGC authority not only to raise premiums, but to set them at different rates, depending upon how it assessed the risk of any given insured company. That would mirror a decades-old approach that the Federal Deposit Insurance Corp. takes with banks, setting premiums based on what it determines is a bank's risk of failure.

"The risk is there, whether the premiums are charged or not. And right now the risk is being borne by the federal taxpayers," Jacob Lew, the White House budget director, recently told McClatchy. "And after a very unhappy experience with bearing that risk (in the national housing meltdown), this is an attempt to try to recalibrate, to say we want to reduce the risk that there's a need for a federal bailout. We want to give the program the ability to fund itself to cover these risks."

That's important, because current PBGC premiums spread the cost among all participants, but effectively allow irresponsible companies to be subsidized by responsible ones.

Since companies that fail to fully fund their pension plans aren't punished, they enjoy an implicit government backstop. (That's similar to what conservatives have criticized as a market-distorting government backstop from mortgage finance giants Freddie Mac and Fannie Mae.)

One key obstacle to the administration's PBGC plan is the U.S. Chamber of Commerce, the powerful lobby for American business and very influential, especially with Republicans in Congress.

"We oppose it," said Aliya Wong, the Chamber's executive director of retirement policy. She said that having the government determine which companies are most at risk would be an undue interference in the marketplace. "If the PBGC comes in and a company is not creditworthy, it influences others to see it that way."

The Chamber isn't opposed to higher premiums, Wong said, just to having government determine the creditworthiness of companies.

However, the FDIC has worked with risk-based premiums for decades, determining what individual banks or thrifts should pay into a pool that reimburses depositors in the event of a lender's failure. The FDIC also places banks on "watch lists," not disclosing the names of institutions on them unless they fail and are subject to intervention.

The PBGC is governed by a three-member board comprised of the secretaries of Labor, Commerce and Treasury. Since 1980, the board has met only 23 times, and not once from February 2008 to February 2010, a period that spanned most of the Great Recession.

"The fact that PBGC's board of directors has only recently begun to meet to discuss these problems is less than reassuring," the GAO report concluded.

"The participation in PBGC has been underpriced for a very long time," said Lew, the budget chief. "This is really a way of calculating the risk and attaching a premium to the entities that get the benefit of the insurance rather than having it be borne more broadly by other taxpayers."

ON THE WEB

MORE FROM MCCLATCHY

Why employee pensions aren't bankrupting states

State budget battles fuel debate about who pays

McClatchy's probe into roots of financial crisis, a Pulitzer finalist

To ask a question about this story or any economic question, go to McClatchy's economy Q&A

For more McClatchy politics coverage visit Planet Washington

This story was originally published March 7, 2011 at 5:06 PM with the headline "Business fights Obama's fix for sick corporate pensions."